What You’ll Learn

Many people struggle with how to budget your income because it feels overwhelming and complicated. The 50/30/20 rule offers a simple budgeting method to help you manage money wisely—without spreadsheets or stress.

In this guide, you’ll see how does the 50/30/20 rule work, real examples and tips to make it fit your life—no matter your starting point.

Key Takeaways

- 50/30/20 rule splits after-tax income into needs, wants, savings.

- Use 50/30/20 rule example monthly income tables to visualize.

- Adjust 50/30/20 rule percentages for high costs or low income.

- How to track 50/30/20 budget: Apps + weekly checks.

- Add frugal challenges like batch cooking for bonus savings.

- Delivers long-term financial security and peace of mind.

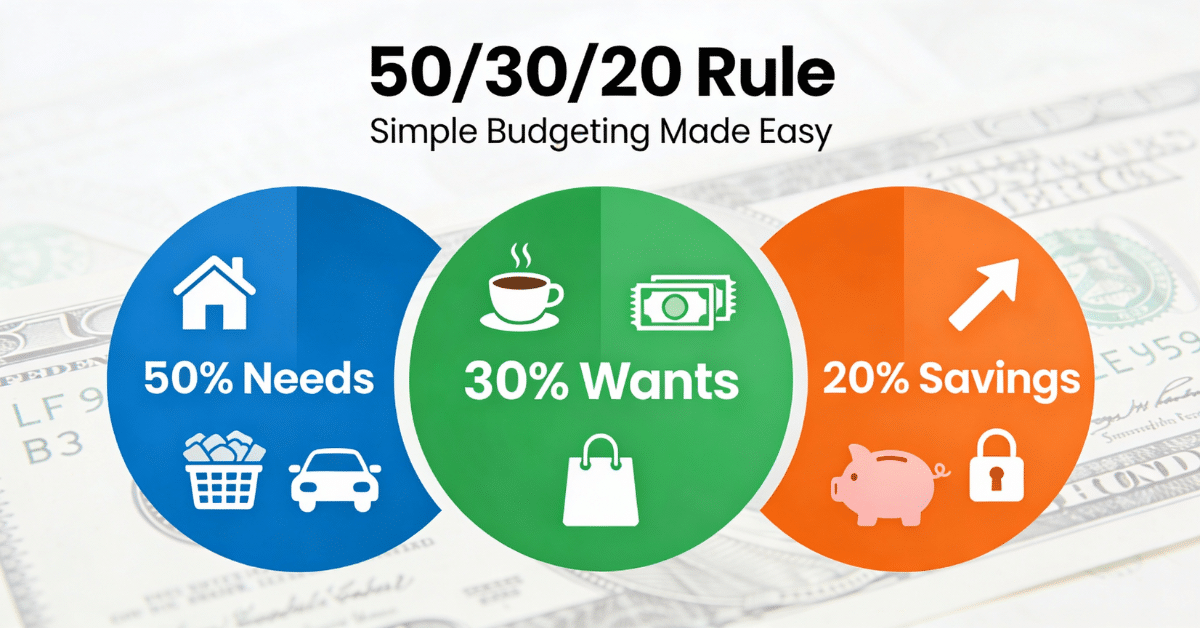

How Does the 50/30/20 Rule Work?

The 50/30/20 rule divides your after-tax income into three clear buckets:

- 50% for Needs – Must-haves like rent, groceries, utilities, insurance, and transport.

- 30% for Wants – Enjoyable extras like dining out, hobbies, or streaming subscriptions.

- 20% for Savings and Debt – Building your future with emergency funds, retirement contributions, or extra payments on loans.

50/30/20 rule example monthly income for $4,000 take-home:

| Category | Percentage | Amount | Frugal Tip |

|---|---|---|---|

| Needs | 50% | $2,000 | Batch-cook meals to cut grocery bills by 20–30%. |

| Wants | 30% | $1,200 | Check save money hacks for easy subscription audits. |

| Savings/Debt | 20% | $800 | Auto-transfer on payday to high-yield savings (4–5% APY). |

This setup keeps things balanced and easy to follow.

Step-by-Step: Implement the 50/30/20 Rule Today

Step 1: Calculate Your Take-Home Pay

Add up your monthly salary after taxes, deductions, and any side income. Tools like a 50/30/20 budget calculator (free online) make this instant.

Step 2: List Your Expenses

Track one month’s spending. Categorize everything—groceries in needs, Netflix in wants.

Step 3: Apply Percentages and Adjust

Multiply your income by 50%, 30%, 20%. If needs overflow, negotiate bills or downsize.

Real talk: It might take 2–3 months to settle in, but consistency pays off.

Real-Life 50/30/20 Rule Example Monthly Income

Single Person in US/UK ($3,000 Take-Home)

- 50% Needs ($1,500): Rent ($900), groceries ($300), utilities ($200), transport ($100).

- 30% Wants ($900): Gym, coffee, weekends out.

- 20% Savings ($600): Roth IRA or student loans.

Frugal challenge: Skip takeout once a week—saves $40/month.

Family in Canada/Australia ($6,000 Take-Home)

- 50% Needs ($3,000): Mortgage ($1,800), childcare ($800), food ($400).

- 30% Wants ($1,800): Vacations, kids’ activities.

- 20% Savings ($1,200): RESP or superannuation.

Unique tip: Shop Aldi or Lidl for 15–25% grocery savings in these markets.

Is the 50/30/20 Rule Realistic?

Yes for most, but adjust 50/30/20 rule percentages smartly.

- High cost of living (e.g., Toronto, London)? Needs to 60%, wants to 20%, savings 20%.

- Low income starters? Begin at 50/30/20 or ease into 50/35/15.

Pro insight: In pricey areas like Sydney or NYC, cap rent at 25–30% via roommates—unlocks 5% more for savings.

How to Track Your 50/30/20 Budget

- Apps: Mint, YNAB, or PocketGuard for auto-categorization.

- Spreadsheet: Google Sheets template with formulas.

- Habit: Sunday 10-minute review—adjust before month-end.

Power move: Link bank alerts for when you hit 80% of a category.

Long-Term Wins from the 50/30/20 Rule

Stick with it for 6 months and watch:

- Emergency fund hits 3–6 months’ expenses.

- Debt drops faster with focused 20%.

- Less stress from automatic decisions.

Many users report feeling in control—plus extra cash for goals like travel.

Frequently Asked Questions

Q: Does the 50/30/20 rule use gross or net income?

A: After-tax income only—keeps it realistic for bills.

Q: Is the 50/30/20 rule realistic for high cost of living areas?

A: Tweak to 60/20/20 if rent spikes—still builds savings.

Q: How do I use the 50/30/20 rule for low income?

A: Scale savings down to 10% at first, ramp up as habits stick.

Q: Can I adjust the 50/30/20 rule percentages?

A: Yes—40/30/30 boosts savings; flexible for life changes.

Q: How do I track my 50/30/20 budget each month?

A: Mint/YNAB apps or Sheets—set alerts for overspends.

This article is for informational purposes only and is not financial advice. Always review your situation before making budgeting or savings decisions.